Never outliving our retirement savings

Protection from Chronic Healthcare risks

Social Security Analysis and Optimization

How will our future Social Security be impacted?

Estate Planning Myths and Options

Leaving a legacy for our families.

At M3 Wealth, our job is to simplify your retirement planning. We do this by providing proven easy to follow steps to help you overcome and prepare for the significant events that may affect your retirement.

WHAT ARE THE TWO BIGGEST CHALLENGES IN RETIREMENT??

1) Outliving our Income!

2) The cost of Healthcare or Long-term Care!

Schedule and Complete your COMPLIMENTARY “Retirement Planning Appointment”

and get… Patrick Kelly’s best-selling book; Stress-Free Retirement as our FREE gift!

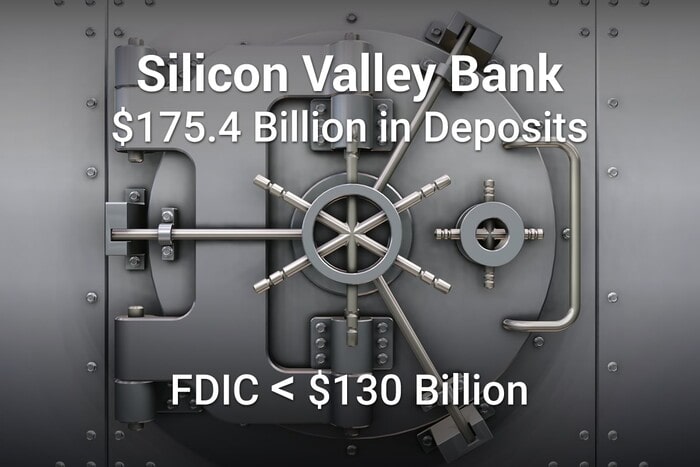

The bank may not the best place to keep our long-term/retirement funds!

Safety & Liquidity

Is the bank a safe place for long-term cash?

Does your bank reserve more than 10% of your deposit?

Do you believe you will get “all” of your Savings/CD’s money in a banking crisis?

Are your bank’s savings rates above 5% currently? (2023)

Is liquidity more important to you than safety in retirement?

If you answered “no” to more than one of these questions or you don’t know the answer, you can get the answers at one of our “FREE” Educational Workshops, or you can “Schedule an Appointment for a FREE Consultation!)

Do your current accounts provide guaranteed income in retirement?

Are you confident you won’t outlive your income in retirement?

Is the income you’ve set aside adequate to cover your chronic healthcare or nursing home expenses in retirement?

Does your current retirement income increase after you retire?

Do you have a plan for inflation and changes to social security?

If you answered “no” to more than one of these questions or you don’t know the answer, you can get the answers at one of our “FREE” Educational Workshops, or you can “Schedule an Appointment for a FREE Consultation!)

Without crop insurance, a farmer can be exposed to unnecessary losses!

Social Security

Without crop insurance, a farmer can be exposed to unnecessary losses!

Social Security

Is Social Security timing important to your Retirement Plan?

Is our Social Security likely to change in 2033?

Is your Social Security taxable?

Will COLA (cost of living increases) be impacted in the future?

Is Social Security going to factor into your retirement?

If you answered “yes” to more than one of these questions or you don’t know the answer, you can get the answers at one of our “FREE” Educational Workshops, or you can “Schedule an Appointment for a FREE Consultation!)

Are you worried about market volatility in Retirement?

If you had to wait 5 years to recover your “market” losses is that an issue?

Are you worried about how to get guaranteed income from your investments?

Are you worried about outliving your retirement income?

Is the cost of Chronic Healthcare in retirement keeping you up at night?

If you answered “yes” to more than one of these questions or you don’t know the answer, you can get the answers at one of our “FREE” Educational Workshops, or you can “Schedule an Appointment for a FREE Consultation!)

The market works, if you have the time or the resources to ride the wave!

IRA & 401(k) Ideas:

Is this money at RISK, and how can we protect our retirement “Nest Egg”?

IRA/401(k) Ideas

Does your current Retirement Plan address the possibility of higher taxes on your IRA and 401k money?

Have you discussed the possible impact of the “Secure Act” on your assets and the assets you hope to pass on to your heirs?

Is an Inherited IRA” a better option than a “Spousal IRA” for you?

Can your children spend your IRA/401k whenever they want?

If you Transfer or Rollover your IRA/401k assets, are they taxed?

If you answered “no” to more than one of these questions or you don’t know the answer, you can get the answers at one of our “FREE” Educational Workshops, or you can “Schedule an Appointment for a FREE Consultation!)

Do you feel like Income Taxes are going to go up in the future!

Are you worried about the impact of taxes on your Retirement?

Were you aware that your Social Security can be taxed?

Are you concerned about taxes on your IRA and 401k?

Are you nervous about how the “Secure Act” could impact your retirement?

If you answered “yes” to more than one of these questions or you don’t know the answer, you can get the answers at one of our “FREE” Educational Workshops, or you can “Schedule an Appointment for a FREE Consultation!)

Important: The information contained on this website is provided for informational purposes only. All articles, charts, brands, logos, names, or other information used is the sole property of the parties cited or referenced. The information on this website should not be construed as investment, legal, or tax advice. M3 Wealth is in no way attempting to provide investment advice. Any use of this information is the direct responsibility of the reading party and should be reviewed and discussed with their financial advisor, attorney, or CPA prior to implementation and/or use. The information contained on this website cannot be used, altered, or distributed, without the express written consent of M3 Wealth.